|

401(k) accounts are meant for retirement, making it difficult to withdraw money. For example, the IRS states the following[1]: Generally, distributions of elective deferrals cannot be made until one of the following occurs:

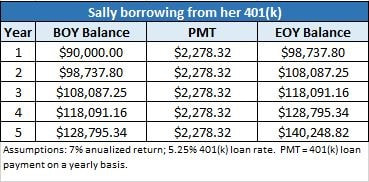

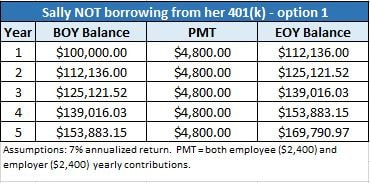

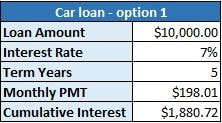

And if you decide to challenge the rules, any money withdrawn will be taxed as ordinary income, in addition to a 10% penalty. In a perfect world, an individual would leave their 401(k) alone until retirement, but we all know that’s not realistic and individuals may need access to their funds, even if it is temporary. To assist, Congress created relief for employees via the 401(k) loan, which allows employees to take loans directly against their 401(k) or other qualified plan balances, subject to certain restrictions. So, let’s dive into the structure and some of the basics surrounding 401(k) loans. The Basics Does every 401(k) plan offer a loan provision? The rule allows for 401(k) plans to permit loans; however, not all plans allow for loans to be taken. Meaning, it is up to the plan’s creator to design the plan with a loan provision. How much can I loan from my 401(k)? Typically, you can borrow up to 50% of your vested account balance up to a maximum of $50,000. For example, if your vested account balance is $80,000, you could borrow up to $40,000 as 50% of your account balance did not exceed the $50,000 maximum limit. In addition, if your vested balance is $20,000 or less, you may borrow up to $10,000, even if it exceeds the 50% threshold. So, if your vested account balance is $8,000, you may borrow up to $8,000. Must I pay interest and if so, who receives the interest payments? Yes, qualified plans are forced to charge a “reasonable” interest rate for 401(k) loans. Most plans deem “reasonable” as the Prime Rate plus 1% or 2%. For example, in today’s environment you are looking at a 5.25% to 6.25% rate, as the Prime Rate is 4.25% (as of 8/29/2017)[2]. The person receiving the interest would be the employee. Meaning, you are loaning from yourself and then paying yourself back your principal, plus interest. How much time do I have to pay back my loan and are there restrictions to the structure of the repayment plan (i.e. interest-only with a balloon payment at the end or can you prepay your loan)? The IRS states an employee must repay the loan within five years[3], that the loan repayment must be in substantially level payments, paid at least quarterly, over the life of the loan. You can NOT structure the repayment plan as interest only with a balloon payment at the end. However, you can pay the principal and interest in full before the end of the five period without penalty (remember you are paying yourself back). What happens if I am unable to pay back the loan due to resignation, being fired, laid off, etc.? If you are unable to pay back the loan, you would have to pay the loan in full[4] within 60 days[5]. If not, and you are younger than age 59 1/2, then the total loan amount taken will be considered a distribution and will be taxed as ordinary income, in addition to a 10% penalty. If you are older than 59 1/2, it will still be considered a distribution and will be taxed as ordinary income, but the 10% penalty will NOT apply. During the repayment of the loan, are the contributions and/or the interest tax deductible and will I still receive my employer’s match? The contributions being made to repay a 401(k) loan are NOT tax deductible and would NOT qualify for an employer match. The interest portion of your loan is also, NOT tax deductible. Depending on the plan, you may not be eligible to make contributions above and beyond your loan repayment amount. Meaning, you may lose out on potentially five years’ worth of matching contributions from your employer. However, some plans do allow for contributions in addition to your loan repayment amount. If your plan allows this, the amount not characterized as a loan repayment IS tax deductible and IS eligible for your employer’s 401(k) match. The true cost behind 401(k) loans Now that we understand the basic structure of a 401(k) loan, it’s time to dive into the true cost of such a loan and the best way to do so is to tell a story about Sally. Sally is an employee of HIJ company. HIJ provides a 401(k) plan for their employees and provides the option to loan from their vested balances. The current “reasonable” interest rate is 5.25% (Prime Rate plus 1%). HIJ match’s 100% of their employees’ contributions up to 3% of the employee’s gross salary. Also, the plan does NOT allow for contributions above the loan repayment amount. Sally currently contributes 3% of her gross salary in order to receive HIJ’s 3% match, equaling a total contribution amount of $4,800 per year (Sally’s annual contribution of $2,400 + HIJ 3% match of $2,400 = $4,800 per year), and her current vested balance is $100,000. Sally would like to buy a new car, but needs an extra $10,000 to close the deal. She has two options: 1) borrow from a bank at a 7% interest rate over five years, or 2) borrow from her 401(k) at a 5.25% interest rate over five years. Sally assumed her 401(k) would grow at an annualized rate of 7%, as it is close to the historical real rate of return[6] of the S&P 500. When Sally looked at her options, she decided to go with option 2 and borrow from her 401(k), as the interest rate was lower. In addition, she thought “Why not? The 5.25% interest is going to me anyway” she felt it was a no-lose scenario. Let’s break down the true cost to Sally’s decision as she missed a few key points.

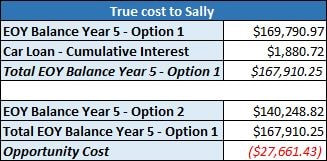

So, what did Sally’s choice truly cost? Let’s look at her projected 401(k) balance at the end of year five after taking a $10,000 loan beginning in year one.[9]  After five years Sally’s 401(k) balance would total $140,248.82, a total gain of $50,248.82 over five years. Not too shabby, and she didn’t even have to pay someone else interest. However, before we get too excited, let’s examine what her opportunity cost was by not going with option 1.    By neglecting to take into consideration the three points covered earlier, Sally’s true borrowing cost was $27,661.43! Even though the 401(k) loan’s interest rate was 1.75% lower than the traditional loan’s rate, losing her employer’s match of $2,400 per year and missing out on the opportunity to allow her funds to grow at an annualized compounded rate of return of 7% ended up costing Sally a rather significant amount.

Conclusion Sally obviously didn’t speak with LBW before making such an impactful decision and in the end, it cost her money. In all seriousness, we recognize we created a story to show the potential damage that could be made by not taking a deeper look when making a financial decision. Our objective is to shed light on the intricacies of a 401(k) loan and provide an example emphasizing the importance of evaluating a financial matter from a holistic level. Too often do we hear individuals making decisions based on superficial research, as Sally did with the interest rate. When it comes to finance, understanding a topic on the surface has the potential to get you into hot water fast. We encourage our clients, prospects, and passersby to reach out and use us as a resource. So, please, if you are reading this and need a sounding board on any financial-related topic, reach out - we do not want to see you fall into poor Sally’s situation. Sincerely, LBW [1]https://www.irs.gov/retirement-plans/plan-participant-employee/401k-resource-guide-plan-participants-general-distribution-rules [2] http://www.bankrate.com/rates/interest-rates/prime-rate.aspx [3] There is an exception when buying a home. https://www.irs.gov/retirement-plans/plan-participant-employee/401k-resource-guide-plan-participants-general-distribution-rules [4] Includes principal and interest. [5] Some plans will allow you to continue making payments after separation from the employer. Again, this is plan dependent. [6] http://www.investopedia.com/terms/r/realrateofreturn.asp [7] We assumed Sally would not repay her loan early and take the full five years for repayment. In addition, we recognize there is an added cost as Sally would not receive a tax deduction for her repayment contribution. For simplicity purposes, we decided not to include this variable. [8] Based on Sally’s assumption. [9] “BOY”: Beginning of Year; “EOY”: End of Year Comments are closed.

|

Archives

June 2018

DisclaimersCopyright © 2018 Leach, Bickmore & Weiss Wealth Management, LLC. All rights reserved.

|

RSS Feed

RSS Feed