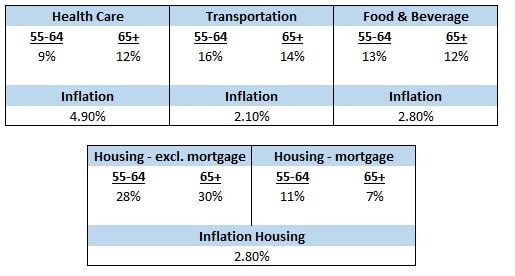

When a family or individual approaches us to begin assessing their ability to retire and live on a fixed income, we explain that financial planning comes down to a simple equation: income (I) – expenses (e) = free cash flow (FCF). Where things become subjective and more complicated is the composition of I and more specifically E. A subjective piece to E, is the rate at which it is increasing over time, otherwise known as inflation. One metric used to describe inflation is the Consumer Price Index (CPI)[1], which measures the rate of change for a basket of goods and services purchased by households. CPI is a general indicator of the rate at which E is increasing over time. The issue – not every E category is inflating at the same rate. Furthermore, each E category has a differently weighted percentage relative to E. Meaning, averaging CPI over time and applying that percentage across all E categories may produce results that are not indicative of the future. To produce a more accurate picture, you must understand the amount you will be spending for each E category and then apply an appropriate inflation rate[2]. Moving forward, one E category one must truly understand is healthcare. The U.S. healthcare system has been front and center for most Americans in recent years and rightfully so, as it affects everyone regardless of their economic status. There are endless debates if our system is broken or not, and what should or should not be done to get it fixed. However, it seems both sides can agree on one thing – the cost of care is increasing at an unsustainable rate. In addition, the percentage amount spent on healthcare is increasing relative to E, slowly moving its way into the discussion as a “game changer” as it pertains to E while in retirement. This is evident in the chart[3][4] below.  Individuals are spending more on healthcare as they enter their later years. Logically, this makes sense, as we tend to need more medical attention as we age. In comparison, three of the remaining four categories decrease as we age, lessening the overall impact to our E. Furthermore, the inflation rate of healthcare is roughly 2% higher than food and beverage, housing, and transportation. The difference in inflation may seem miniscule; however, it’s not, as seen below[5].  At the end of 10 years, you would be spending almost $3,000 more per year in healthcare costs. If you assumed you were 75 at the end of the 10-year period, were going to live another 10 years, and held the cost of healthcare constant, you would pay, roughly, an additional $28,000 more in healthcare due to a 2% difference in the inflation assumption. And to make matters worse, pundits believe the total cost of Medicare will increase 6.5%[6] per year – 1.6% higher than the average cost of healthcare!

Now that we understand the impact of healthcare cost to our overall E, what can a family or individual do to help mitigate some risk? Utilize qualified vehicles such as a Health Savings Account (HSA). An HSA is a powerful vehicle to use when planning for medical expenses pre- and post-retirement (you can re-read our May 2016 blog post titled HSA’s, FSA’s, HRA’s…“Whoop-de-doo! What does it all mean, Basil?” for further information). If you are currently retired and on Medicare you are unable to contribute to an HSA. However, if you have an HSA balance, you can use it for any qualified medical expenses. If you are not retired and your current healthcare plan qualifies you to contribute to an HSA, you could fully fund the account until you are no longer allowed to, and then utilize it while on Medicare to help cover some unknown costs in retirement. It is a great vehicle to help mitigate future increases in cost. Understand each part of Medicare and what it covers, then fill in the gaps with supplemental insurance (Medigap policy). Understanding what Medicare Part A, B, C, and D all cover is important because they most likely will not cover all medical costs. To fill the gap, you may buy what is referred to as a Medigap policy. This policy is meant to fill the holes in which Medicare leaves. This will help mitigate out of pocket expenses you may incur while in retirement. Moreover, your premiums will increase over time, as explained above, but it is easier to predict the rise in premiums then having to pay out of pocket for an unexpected event for which you were not covered. We would highly suggest you work with an independent insurance broker who can help facilitate quotes and provide customized advice on how you should be covered. Please note, every family or individual has different circumstances – what works for your neighbor may not work for you. Understand the future cost of healthcare and plan appropriately. Understanding the future cost of healthcare and the amount you may spend is paramount. With the assumption that costs can change, as they are highly unpredictable, being conservative with your inflation rate and spending assumptions will help stress test your scenario, allowing you to plan for future costs. In addition, continually reviewing these assumptions and adjusting accordingly will help with the ever-changing landscape of healthcare costs. Healthcare is on the rise and until there are changes to our current healthcare system, plan on this being an issue for the foreseeable future. Sincerely, LBW [1] https://en.wikipedia.org/wiki/Consumer_price_index [2] One may calculate a weighted average inflation rate and apply it to the overall E in our equation, instead of inflating each category at a different rate. [3] JP Morgan Asset Management. (2017). Guide to Retirement 2017 Edition [PowerPoint slides]. Retrieved from https://am.jpmorgan.com/us/en/asset-management/gim/adv/insights/guide-to-retirement [4] Inflation metric for housing is a general metric as there is not a specific inflation metric for “Housing – excl. mortgage” and “Housing – mortgage”. [5] LBW Wealth Management [6] JP Morgan Asset Management. (2017). Guide to Retirement Health care module [PowerPoint slides]. Retrieved from https://am.jpmorgan.com/blob-gim/protected/1383355049261/83456/2017%20GTR%20Health%20Care%20module_final.pdf?segment=AMERICAS_US_ADV&locale=en_US Comments are closed.

|

Archives

June 2018

DisclaimersCopyright © 2018 Leach, Bickmore & Weiss Wealth Management, LLC. All rights reserved.

|

RSS Feed

RSS Feed