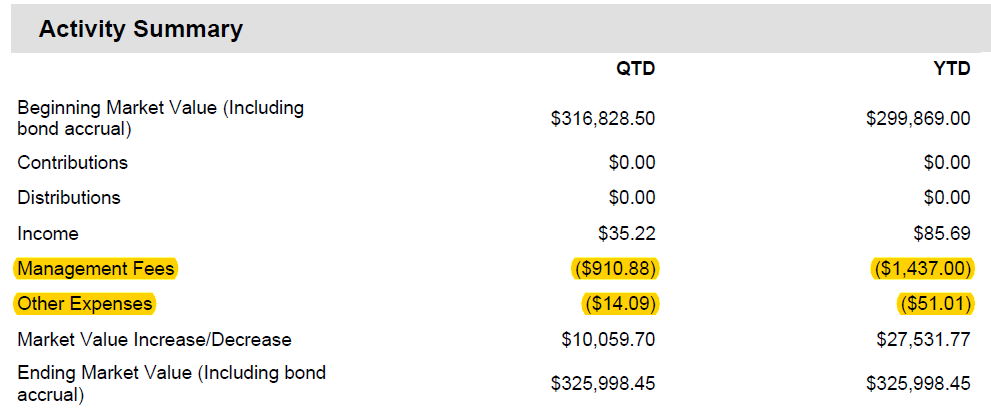

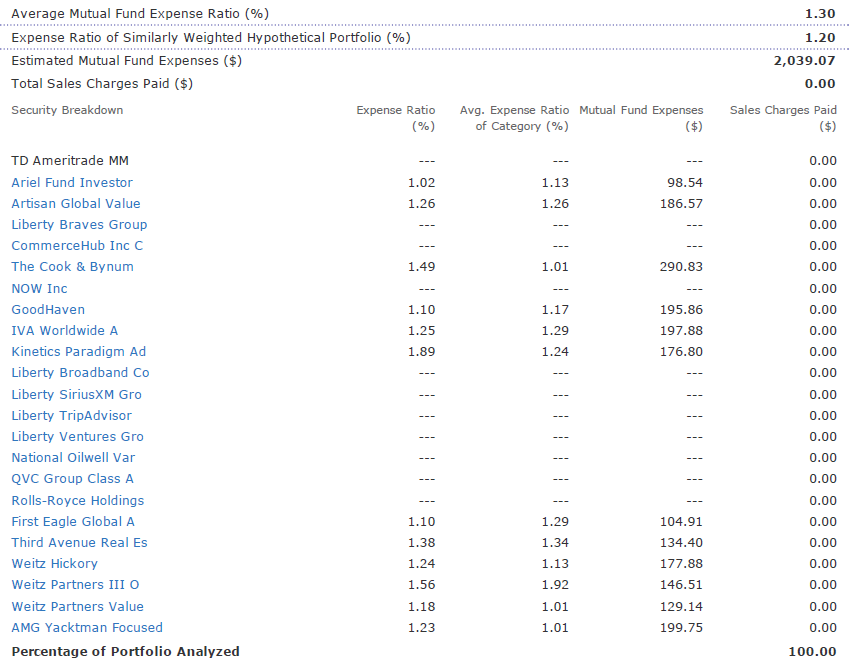

Recently we came across an article, by the wonderful author Andrea Fuller of the Wall Street Journal (WSJ), titled “What’s My Investing Fee? A Frustrating Quest”. After reading it, we were compelled to write a response to Ms. Fuller. Our intention – to provide proof not all investing fees are so nontransparent. Before you move forward we kindly ask our readers to do a bit of work. If you could please read the article below and then read our response, we would greatly appreciate it. We hope you enjoy it as much as we did putting it together. https://www.wsj.com/articles/whats-my-investing-fee-a-frustrating-quest-149420982 Response My name is Tim Bickmore, I am Co-Founder/Financial Advisor at LBW Wealth Management, a Registered Investment Advisor (RIA) based in Madison, WI. I stumbled across your article this morning on “WSJ Wealth Adviser Briefing” and couldn’t help but reach out and express my sincere empathy and frustration. The transparency of my industry is almost as clear as a greasy hamburger wrapper (and I am being generous). Add in high-pressured sales and a litany of jargon, and you get an industry myself and my firm are not proud of. Our disregard for how our industry is viewed is why we started our firm - “To transform the perception and utilization of wealth management and wealth development.” My industry’s nontransparent nature is slowly changing, but not fast enough. I empathize with your story as it is the norm. I am writing this email to provide a glimmer of hope that not all “Financial Advisors” are made equal. Without further ado, below is a description on how we explain fees to our clients. 1. LBW Wealth Management Fee a. LBW charges an annual fee based on the assets under our management (AUM). To clarify when we say, “assets under management” we mean the assets we are actually managing. For example, a client may have a $1,000,000 net worth and we will advise on the client’s real estate property, employer-sponsored plan, etc. If the client has a $10,000 rollover IRA we manage for them, the AUM fee would not apply to the client’s real estate or employer-sponsored plan even though we are advising on those assets. Our fee schedule is as follows and can be found in our ADV Part 2A. b. Assets Under Management Annual Fee i. First $500,000 = 1.25% ii. Next $500,000 = 1.10% iii. Next $1,000,000 = 1.00% iv. Next $3,000,000 = 0.85% v. Next $5,000,000 = 0.70% vi. Amounts in excess of $10,000,000 = 0.50% 2. Custodial Transaction Fees When implementing portfolios, there are transaction costs. For example, at our current custodian, TD Ameritrade, it costs $6.95 for each equity trade. For certain mutual funds, there is a possible $24 transaction cost. This is an additional cost to our clients, which we take into consideration when making trades. 3. Expense Ratios Mutual funds have different types of fees associated with them. You have load fees, expense ratios, 12b-1 fees, etc. The mutual funds we invest in are “no-load funds”. So, the expense ratio is the only other expense incurred by our clients. 4. Providing our Clients with Clarity We could explain our fees until we are blue in the face, but as you eluded to in your article – you just want to see how much you are paying. Below are screenshots of a client report. The first picture shows “Management Fees” which is the actual amount our client has paid us, and “Other Expenses” which is the amount the client has paid to our custodian (the transaction fees) for Quarter to Date (QTD) and Year to Date (YTD). The second picture clearly presents the “Average Mutual Fund Expense Ratio” and the “Estimated Mutual Fund Expenses”. Beneath those numbers, you see a breakdown for each holding and its respective expense ratio and anticipated $ value based on the fund’s $ amount.   Every penny our client is paying is clearly laid out and transparent. Unlike the firm you discussed in your article, we are not large. However, with limited resources in comparison to the aforementioned firm, we are able to spell out all fees charged to our clients to the $ amount, with little effort. Therefore, I wanted to email you, to provide proof that your experience may be the norm, but it sure doesn’t have to be. As you can see we are trying to hold true to our “Why”, and hopefully one individual, family, and/or business at a time we will change the perception of our industry.

End of our response To Sum Up The nontransparent nature of Ms. Fuller’s journey, in our opinion, was in part purposeful and part bureaucracy with plenty of miscommunication in between. However, the amount of work put into understanding her fees is inexcusable on all levels and only helps fuel the negative reputation of our industry. Our goal was to provide clarity and comfort that Ms. Fuller’s situation does not have to be the norm. As we always say, “you don’t know what good cooking is until you have it” – hopefully you will have experienced a bit of good cooking after reading this post. Sincerely, LBW Comments are closed.

|

Archives

June 2018

DisclaimersCopyright © 2018 Leach, Bickmore & Weiss Wealth Management, LLC. All rights reserved.

|

RSS Feed

RSS Feed