The wave of startups and entrepreneurship is upon us. We have witnessed these companies change work culture, disrupt industries, and make billionaires out of 20-some-year old’s. However, what is less publicized is the rise of stock compensation and its different forms. Historically, this type of compensation was given to individuals who were in upper management positions. Today, some companies are granting stock options to general employees when they are hired. When examining compensation packages of thriving startups, one can find Non-Qualified Stock Options (“NQSOs”), Incentive Stock Options (“ISOs”), Restricted Stock Units (“RSUs”), Stock Appreciation Rights (“SARs”), and other types littered throughout. These various terms are actually quite different, so in this month’s blog, we have decided to address two forms of employee stock options we typically see – NQSOs and ISOs. We lay out the structure of each and at the end discuss our thoughts on when to exercise. What is an employee stock option? Before diving into the details, we first need to understand what an employee stock option is. When an employee is granted stock options by their employer, it provides the employee the right to purchase the employer’s stock at a pre-determined price (exercise price) for a specific time period. For example, let’s say XYZ company grants 10 NQSOs to employee A with immediate vesting. If XYZ’s stock increases above the exercise price, then employee A will participate in the growth of the company. Therefore, employee stock options are typically referred to as incentive compensation. How are NQSOs and ISOs structured? When it comes to NQSOs and ISOs there are four elements that are important to pay attention to. 1. Exercise price

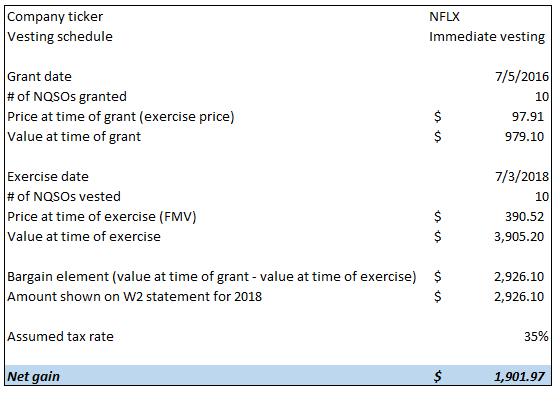

What is the tax liability of NQSOs and ISOs? Now that we understand what to look for, we can dive into the taxation of each type of option. 1. NQSO taxation

How do you exercise? When granted a stock option an employee has the right to purchase said stock at a pre-determined price. For example, if Employee A wanted to exercise 10 NQSOs at an exercise price of $10 per share, then they must buy those shares for $1,000. Now, it may not be difficult to bring $1,000 to the table to exercise 10 NQSOs. However, what if you had 10,000 NQSOs at $10 per share? To purchase your shares, you would have to have $100,000 in cash. Because stock options can become highly valued, there are two primary ways to exercise your options: a cash or cashless exercise. The prior example represents a cash exercise. An individual must bring actual cash to the deal to purchase the stock at the exercise price. As mentioned, this can become difficult as employee stock options can become extremely pricey as they accumulate. However, if your goal is to hold more shares of the company for reasons that we lay out below then bringing cash to the transaction can become advantageous. To mitigate this potential cash outlay, there is another way to exercise, called a cashless exercise. Investopedia provides an excellent explanation. “A cashless exercise is a transaction in which employee stock options are exercised without making any cash payment. Such a transaction utilizes a broker to provide a short-term loan so that the employee exercising the options has enough money to do so. Once the loan to exercise the options is in place, the employee then sells enough shares to pay back the broker for the loan, broker fees and taxes. The person exercising the options then possesses the shares.”[2] Typically, a cashless exercise is the primary choice when exercising employee stock options because many don’t have the cash on hand nor want to liquate other assets to exercise their options. This can become efficient, especially if you want to exercise and then sell immediately. When should you exercise? This is the million-dollar question and, of course, is the most difficult to answer. It can be viewed in multiple different ways from current trading price vs. intrinsic value to your percentage of exposure to the company as it relates to your total investable assets. However, what further complicates this question is that these options are typically given for free and because of this it may cause you to place this money in a “I don’t care; it was money I didn’t have anyways” bucket. Employee stock options can become a large part of your net worth overnight as early employees at Alphabet (Google) or Facebook can probably attest. This mental accounting can force someone to “let it ride” and not examine their total exposure to the company (which can be troublesome as we explained in our February blog “Making the Bet – Part 1: The Game”). With that said, everyone has different circumstances, so to create a blanket statement on when to exercise isn’t prudent. To exercise you must take into consideration exposure, price vs. value, tax liability, etc. The best thing to do is work with qualified professionals to help guide you through this complicated and in-depth decision. At LBW, we would be happy to help work through it with you! Sincerely, LBW [1] Short-term capital gains are taxed at ordinary income tax rates. Long-term capital gains are taxed at long-term rates, which are typically lower than ordinary income tax rates depending upon one’s income tax bracket. [2] https://www.investopedia.com/terms/c/cashlessexercise.asp Comments are closed.

|

Archives

June 2018

DisclaimersCopyright © 2018 Leach, Bickmore & Weiss Wealth Management, LLC. All rights reserved.

|

RSS Feed

RSS Feed