At some point in life you’ve probably thought, “I wish I could get paid without having to go to work.” Luckily for you, that’s exactly what an IRA is for: saving enough money now so that you can pay yourself not to work (commonly known as retirement). To understand how this is done, let’s start with the basics: What is an IRA? IRA stands for “Individual Retirement Arrangement”.[1] Simply put, they are accounts with certain tax benefits, which differ depending on the type of account, for individuals saving for retirement. Although there are several different kinds, we’ll be focusing on the differences between a traditional IRA and a Roth IRA. Traditional IRA Structure: Any contributions that are made to the account are partially or fully tax-deductible, depending on your situation: 1. If you OR your spouse has a retirement plan through work, your deduction might be limited. Follow this link[2] for more details. 2. If you don’t have a retirement plan at work or your income exceeds certain levels, any contributions you make are fully deductible. However, the maximum annual contribution, for 2017 and 2018, to both traditional and Roth IRAs is $5,500 for investors under age 50, and $6,500 for investors over that mark.[3] There are also rules for taking distributions from the account: 1. Any withdrawals from the account are subject to your income tax rate at that time; 2. In general, withdrawals taken before age 59 ½ are subject to your income tax rate as well as an additional 10% penalty. Click here[4] to see the exceptions; 3. After age 59 ½, the investor is free to take any size distribution without penalty Roth IRA Structure: Unlike a traditional IRA, any contributions made to the Roth account are after-tax and cannot be deducted. The implication here is your Roth contributions are taxed at your current tax rate. Because of this, when distributions are taken at retirement, they are not taxed – including any possible capital gains. Roth IRAs also have distribution rules, but they aren’t as restrictive as traditional IRA rules; www.rothira.com sums them up best: 1. “If you are 59½ or over, you may withdraw as much as you want, as long as your Roth IRA has been open for at least 5 years; 2. If you are under 59½, you may withdraw the exact amount of your Roth IRA contributions with no penalties; 3. There are special exemptions for first-time home purchase and college expenses.”[5]

Which IRA is best? As always, the best option is dependent on the individual/household’s situation. That being said, the benefits of both IRAs are largely differentiated by taxes, so we’ve mapped out some scenarios to help get you pointed in the right direction: A Traditional IRA might be more beneficial if: 1. You’re in a high tax bracket now, but expect to be in a lower tax bracket during retirement.

A Roth IRA might be more beneficial if: 1. You’re in a lower tax bracket now, but expect to be in a higher tax bracket during retirement.

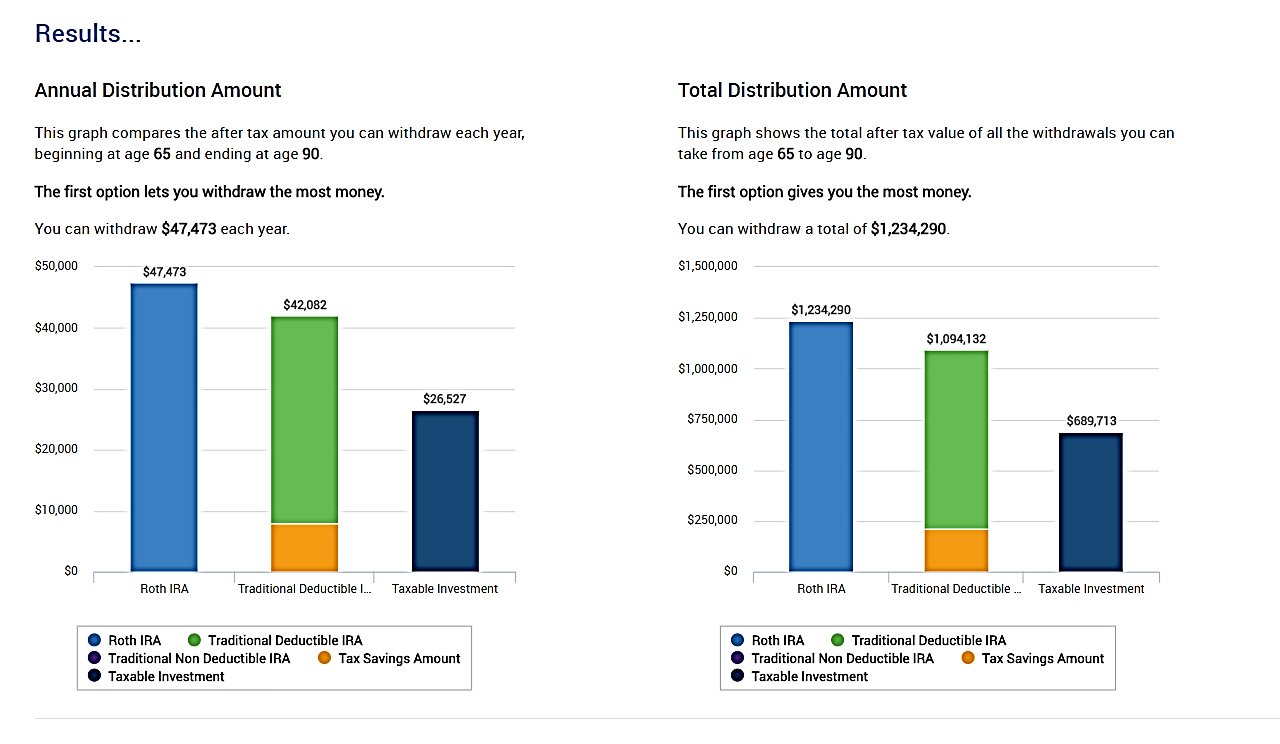

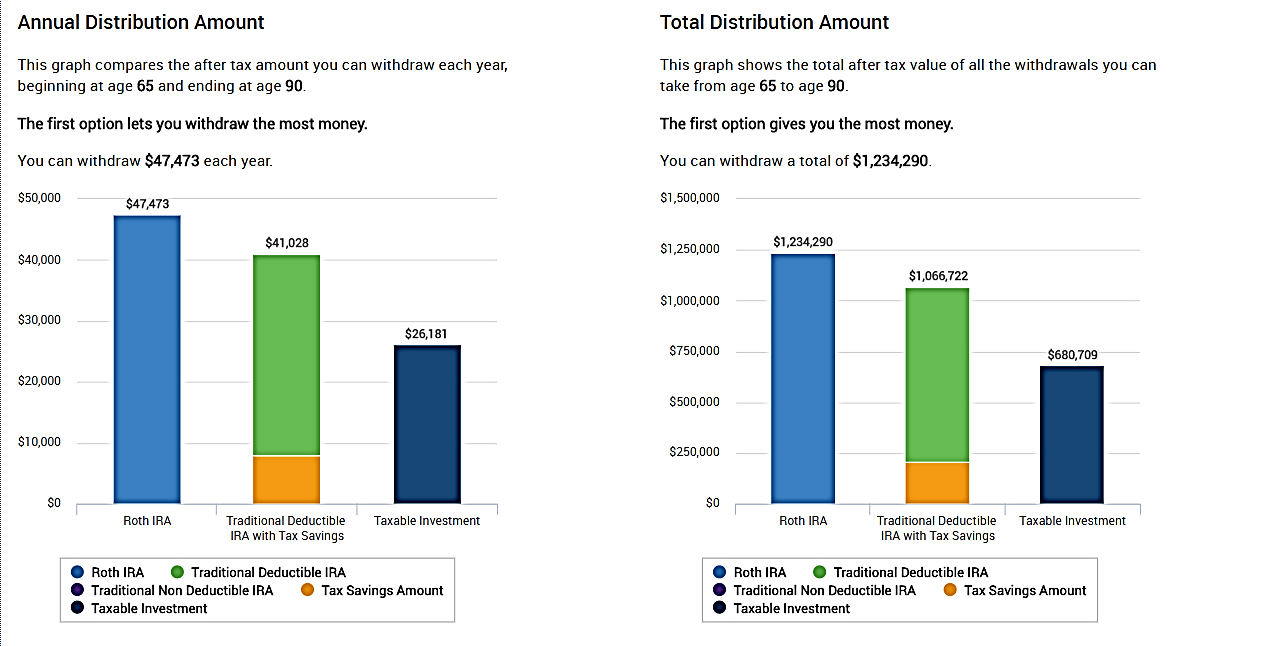

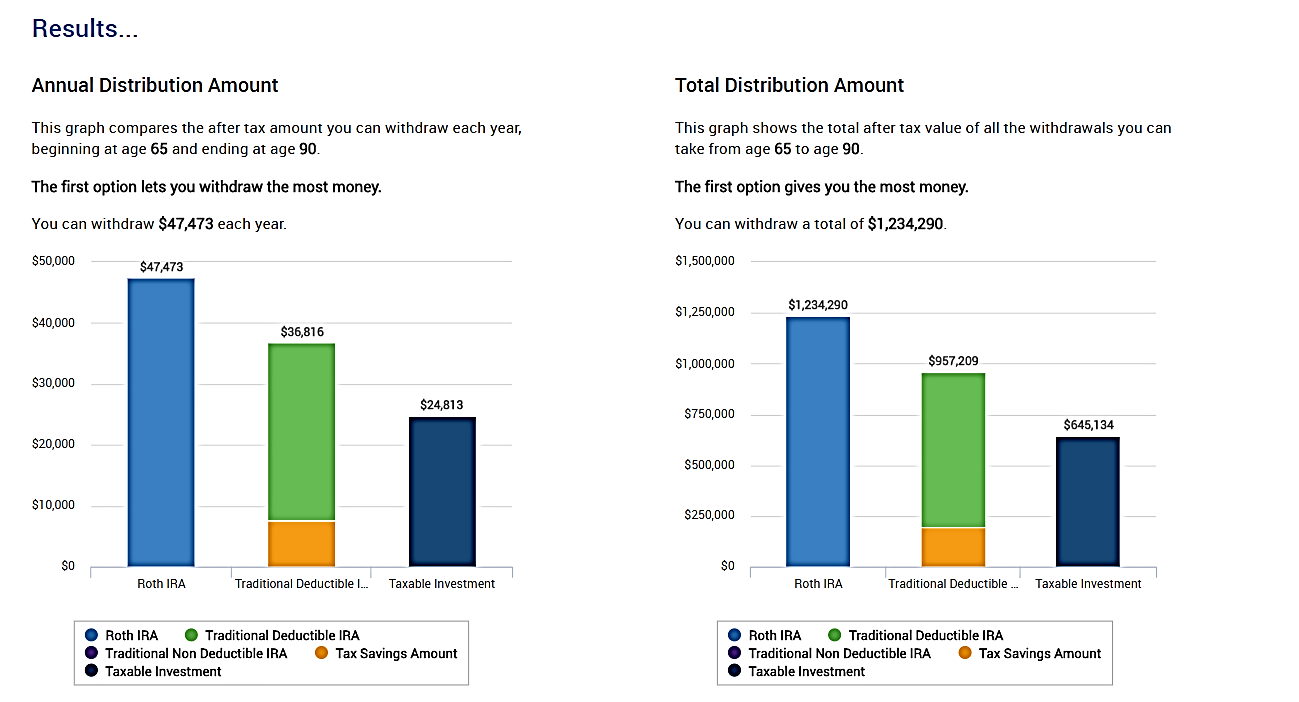

At this point we’ve covered the structures of both IRAs, as well as some scenarios that benefit each. The last few examples provided below should help tie everything together, giving you a visual representation of how the traditional IRA and Roth IRA differ from a numbers’ standpoint. For each of the three examples below, the following assumptions were made: 1. The investor is a 35 year-old male who plans to retire at age 65, 2. He does not have a retirement plan through work, 3. He contributes $5,500 annually to his IRA (the maximum amount allowed if you are younger than 50), 4. He makes $100,000/year, placing him in the 24% tax bracket (new for 2018), 5. His IRA earns a reasonable 7% annual rate of return, and 6. He plans to take distributions from the account from age 65 to age 90. Scenario 1[7]:  In addition to the criteria above, this example assumes that the investor will drop down to the 22% tax bracket during retirement. The chart on the left shows that the Roth IRA is the best value for our hypothetical investor, allowing annual distributions of $47,473 from age 65 to age 90. The total value of the Roth account, shown on the right, is just over $1.2 million. We mentioned earlier that if you have a lower tax rate at retirement than you do now, a traditional IRA could be more beneficial. Even though that can be true, the minor change in dropping from 24% to 22% for this scenario isn’t enough to put it ahead of the Roth account. However, the value of the traditional IRA is the highest amongst the three scenarios, which illustrates the possible advantage it can have given different circumstances. Scenario 2[8]:  This scenario assumes that the investor’s tax rate remains at 24% when they reach retirement. The value of the traditional IRA is slightly lower when compared to Scenario 1, reiterating the benefit it can have by paying a lower tax rate in retirement. As you might have noticed, the value of the Roth IRA hasn’t changed because the investor’s current tax rate remains the same for each example. Scenario 3[9]:  This final scenario assumes that the investor’s tax rate increases to 32% at retirement, producing the most significant impact on the traditional IRA thus far.

Final Thoughts Understanding the differences between these IRAs is just one of many steps in planning for retirement, and we’ve only scratched the surface. The large role taxes play on the benefits of each IRA makes it extremely important to consider how short and long-term changes could impact their value. The same is true of your income stream; if it increases or decreases, how will it influence the value of your IRA? These questions and evaluations are just the tip of the iceberg, but you need not get discouraged! The quality folks at LBW are here to help you make informed decisions that are entirely your own, because the better you understand what your options are, the more comfortable you’ll be with the investment. Thank you for taking the time to read our blog! If you have any questions or comments regarding the information we’ve covered please don’t hesitate to give us a call, your feedback is always appreciated and welcomed. Sincerely, LBW [1] https://www.irs.gov/taxtopics/tc451 [2] https://www.irs.gov/retirement-plans/2017-ira-deduction-limits-effect-of-modified-agi-on-deduction-if-you-are-covered-by-a-retirement-plan-at-work [3]https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits [4]https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-tax-on-early-distributions [5] http://www.rothira.com/roth-ira-withdrawal-rules [6] http://www.rothira.com/roth-ira-withdrawal-rules [7] LBW Wealth Management [8] LBW Wealth Management [9] LBW Wealth Management Comments are closed.

|

Archives

June 2018

DisclaimersCopyright © 2018 Leach, Bickmore & Weiss Wealth Management, LLC. All rights reserved.

|

RSS Feed

RSS Feed